Summary

Gas trade between the European Union and Russia increased considerably in both 2016 and 2017, despite the ongoing political crisis. Simultaneously, two long-standing disputes in the EU-Russia gas relationship – regarding Gazprom’s monopolistic practices and the EU’s third energy package – were settled.

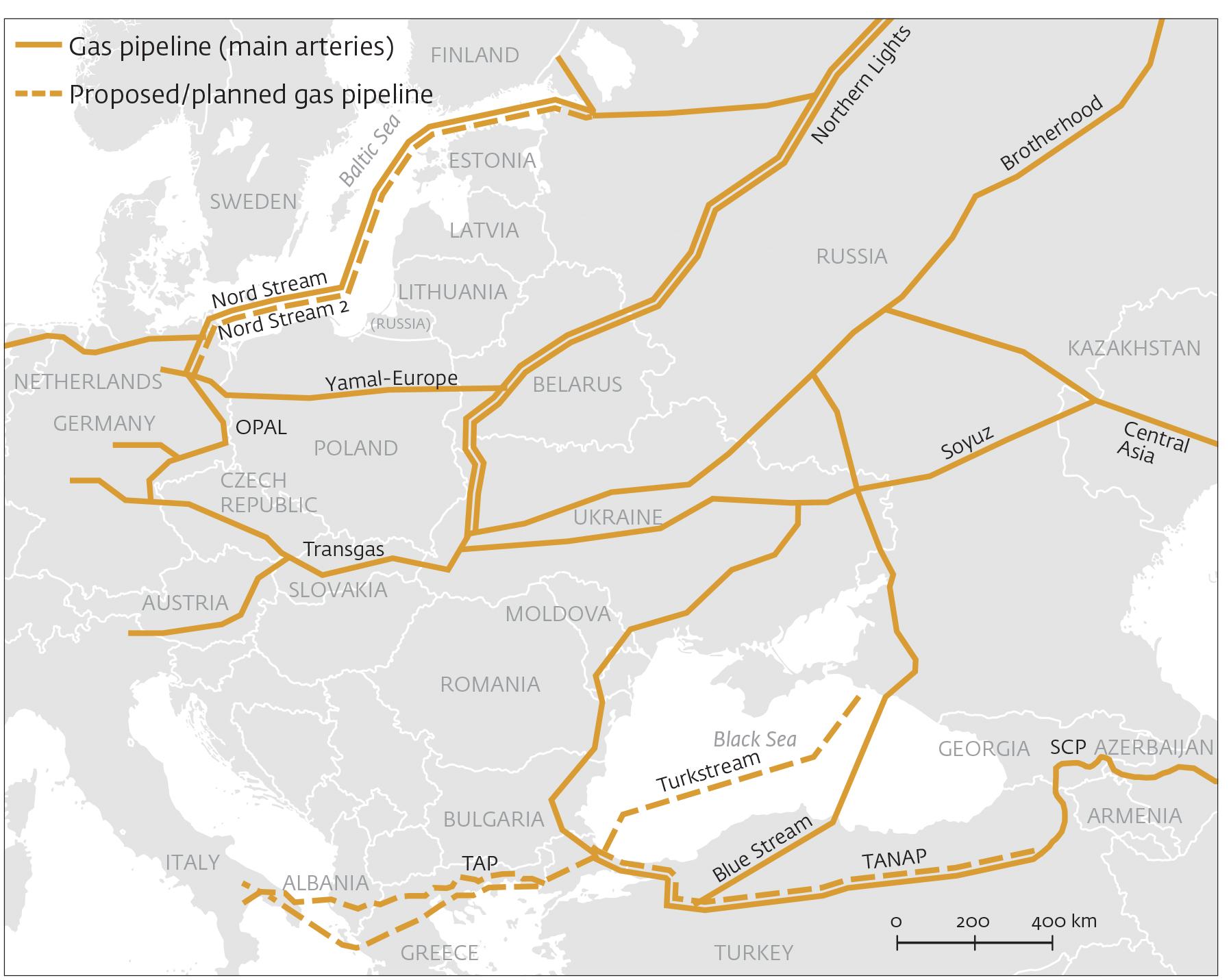

Russian companies have invested in new infrastructural projects for the export of gas to Europe, including the launch of the Yamal LNG terminal in December 2017 and the construction of the TurkStream and Nord Stream 2 pipelines. However, significant challenges remain for the relationship, most notably the intra-EU controversy on Nord Stream 2 and uncertainty about future gas transit in Ukraine.

An agreement between Russia, the EU and Ukraine is possible whereby Nord Stream 2 would be accommodated with contractual guarantees that gas transit in Ukraine will continue. This would also satisfy the commercial requests of Russia’s Southern and Eastern European gas customers.

Russian gas exports to Europe rose to unprecedented highs in 2016 and 2017. According to Gazprom’s delivery statistics, 192.2 billion cubic metres (bcm) of gas were exported to Europe and Turkey in 2017, compared to 178.3 bcm in 2016 and 158.6 in 2015.1 This trend seems to be continuing in 2018, as Russian gas exports to the EU reached a new summertime record.

This performance may appear surprising, given the context of political crises and reciprocal sanctions between the EU and Russia (which have nonetheless left the energy sector largely unscathed). In fact, the rise in Russian gas supplies to Europe is due to commercial and contextual factors that have little to do with politics. The economic recovery in Europe, decreasing gas production in the EU, lower Russian gas prices and the limited availability of non-Russian liquefied natural gas (LNG) in the European market were among the main commercial reasons. Cold winter temperatures and increased coal to gas switching in some European countries also boosted gas demand.

At the same time, the EU-Russia gas relationship has been rendered more predictable by the resolution of long-standing commercial disputes, most notably the European Commission’s antitrust investigation concerning Gazprom, and Russia’s complaint at the World Trade Organisation (WTO) against some key EU market regulations (the third energy package). Moreover, Russia’s main import partners in Western Europe seem happy to continue and even increase their energy purchases from Russia.

In this context, despite the continuation of political tensions with the EU, Russian companies felt confident enough to implement new infrastructural projects for the export of gas to Europe and beyond. This included the launch of the Yamal LNG project in December 2017 and the ongoing construction of the TurkStream and Nord Stream 2 pipelines during 2018.

Nevertheless, important challenges remain for the EU-Russia gas relationship. The Nord Stream 2 project has ignited heated debates within the EU, where some East-Central member states staunchly oppose the project. The United States has intervened in the debate too by threatening to sanction European companies that are involved in the project and advocating its prospective LNG exports as an alternative. Moreover, uncertainty persists concerning the future of gas transit in Ukraine after the expiry of the current contract between Moscow and Kiev in December 2019.

This Briefing Paper reviews these issues and the main developments in the EU-Russia gas relationship. It argues that an agreement is possible between Russia, the EU and Ukraine, which addresses outstanding issues and preserves both the mutually advantageous energy relationship and Ukraine’s role as a transit country.

The surge in Russian gas exports to Europe

From 2015 to 2017, the EU saw considerable growth in gas demand, which reached 548 bcm/year in 2017. This is 76 bcm higher than in 2014 (even though it is still below the peak of 585 bcm reached in 2010).2 Growing demand has been accompanied by decreasing indigenous production, from 300 bcm in 2010 to 250 bcm in 2016. This was mostly due to the progressive depletion of North Sea resources and cuts in production in Groningen, the Netherlands, because of related seismic activity.

Europe’s growing demand for external gas supplies has been satisfied primarily by Russian gas. Following pressure from the European Commission and its customers, Gazprom has partly renegotiated the terms of its supply contracts by adopting market-based pricing in place of oil-linked prices. Together with the rouble’s weakness (which reduces the domestic cost base for Gazprom in US dollar terms), this has made Russian gas more competitive.3

The availability of sufficient reserves and spare infrastructural capacity have also played an important role. While Gazprom was able to sustain increased supplies of gas to the EU, other exporters such as Algeria (the third largest external supplier of gas to the EU after Russia and Norway) saw a 14% decline in pipeline exports in 2017. Not only did Gazprom use the Nord Stream and Yamal-Europe (via Poland/Belarus) pipelines at near full capacity, it also increased the gas it exported via Ukraine by 13.7%, reaching a total volume of 93.5 bcm in 2017, the highest figure since 2011.4

On the other hand, LNG’s competition with Russian gas has been weaker than expected. This was the result of delays in some LNG projects and especially of higher LNG demand in Asia (particularly China), which remains the primary market for LNG due to higher demand and prices. The availability of LNG in the European market began to increase from 2017 and may continue to do so in the next five years depending on demand in Asia. In a scenario of lower Asian demand, LNG from the US (the closest prospective large supplier to Europe) could compete with Gazprom and other supplies via pipelines for some shares of the European market.

Settling disputes: The antitrust and WTO cases

While the recent surge in Russian gas exports to Europe occurred, two key disputes between Gazprom and the EU came to an end. In May 2018, the European Commission ended its antitrust case against Gazprom, having secured substantial commitments from the Russian company on more competitive prices and greater market integration for Eastern European member states.

The Commission had launched the antitrust investigation in 2011 and had accused Gazprom of abusing its dominant market position in Eastern Europe. According to the Commission, Gazprom’s contracts in the region hindered the cross-border flow of gas, which resulted in the fragmentation of the regional market and different prices from country to country.5

In the ensuing negotiations, Gazprom committed to removing contractual barriers to the cross-border flow of gas. It also linked gas prices in Eastern EU members to benchmark prices in Western European hubs. Gazprom’s commitments will adjust prices in Eastern European markets that are isolated due to the lack of infrastructure to market-based prices in Western Europe. They are thus conducive to the further integration of the EU energy market.

By making these commitments, Gazprom has avoided a fine being imposed by the European Commission. However, the Russian company had to make important concessions, and essentially change its marketing strategy from oil-linked contracts to more market-based and, at present, lower prices. Failure to honour the commitments could still lead to Gazprom being fined over the next eight years.

Moreover, in mid-August 2018 the World Trade Organisation published its ruling on Russia’s complaint against the EU concerning certain provisions of the third energy package, duly ending the other main dispute concerning EU-Russia gas relations. The European Commission had introduced the third energy package in 2009 with the aim of integrating the EU’s energy market and increasing competition. One of its central requirements is unbundling the ownership of energy production and supply from that of energy transportation.

In April 2014, Russia had filed a complaint with the WTO about this legislation, arguing that it treated Russian gas and gas transportation services unfairly. However, the WTO ruled that the main principles of the third energy package are lawful. On the other hand, it also stated that some of its aspects were not in line with WTO norms. Most notably, this concerned a 50% cap imposed by the EU on the utilisation capacity of the OPAL pipeline, a land-based continuation of the Nord Stream pipeline, which de facto artificially constrained the use of the latter. The WTO ruling also stated that the EU’s Trans-European Networks for Energy (TEN-E) strategy, which aims at linking the infrastructure of EU members, is inconsistent with WTO law because it provides most favourable conditions for the transportation of natural gas of any origin other than Russian (thus discriminating against the latter).6

Both the EU and Russia issued positive comments about the WTO ruling. The EU was satisfied with the overall WTO assessment of the third energy package. In the years after Russia filed the complaint, Gazprom had largely adjusted its strategy to this new legislation. For the Russian company, the WTO pronouncement on the TEN-E strategy and the OPAL pipeline are seen as the main achievements. The WTO’s view on OPAL strengthens the case for fuller utilisation of the Nord Stream pipeline and can constitute a precedent for the Nord Stream 2 project.

New infrastructural projects: Yamal LNG, TurkStream

While Gazprom’s exports to Europe surged and long-standing disputes came to an end, Russian gas exporters kept working on new infrastructural projects. The first significant one to be completed was Yamal LNG, which is expected to produce 16.5 million tons of LNG per year by 2019. The project was developed by a consortium including the Russian Novatek, the French Total, China National Petroleum Corporation and the Silk Road Fund.

Yamal LNG is significant in several respects. It is the first large Russian LNG project that can export to the EU market (even though most of its gas might in fact go to Asia). It was led by Novatek, a private company, unlike state giant Gazprom. The project was completed on time and within budget despite being targeted by US sanctions. This was possible thanks to Chinese lenders, who swiftly replaced Western investment, and the switching of financing from dollars to euros.7

The TurkStream project also seems to be nearing completion. It will transport 31.5 bcm/year of gas to Turkey and the EU along a route that goes from Russia’s Black Sea coast to European Turkey under the Black Sea. By the end of April 2018, the laying of the first string of the project (with half the total capacity) was completed. Most likely, it will replace Russian gas exports to Turkey that are currently transported via Ukraine and the Balkans.

The second string of the project is under construction and is mostly intended for exports to Southeast and Southern Europe. This section of the project would end at the Turkish-EU border, where it would be linked to EU interconnectors – possibly the planned Poseidon pipeline connecting Greece and Italy, the Turkey-Bulgaria Interconnector, or the Trans Adriatic Pipeline.

Nord Stream 2

Nord Stream 2 is the new Gazprom-led infrastructural project that has aroused more controversy in the EU. With a capacity of 55 bcm/year, it will carry gas from the Russian Baltic Sea coast to Germany via an offshore route running parallel to the already existing Nord Stream pipeline. Following its completion, the total capacity of the Nord Stream route will rise to 110 bcm/year, making it the main export corridor for Russian gas to Europe.8

The project was announced in the summer of 2015 by a consortium including Gazprom, German companies Uniper and Wintershall, France’s Engie, Austria’s ÖMV and Dutch/British Shell. Its proponents argued that Nord Stream 2 will connect Gazprom’s large gas supplies to its bigger customers in Western Europe without transit-related risks and fees. However, the project soon attracted criticism, with opponents arguing that it will consolidate Gazprom’s position in the European energy market, weaken Ukraine’s role as a gas transit country and thus its strategic leverage vis-à-vis Moscow in the ongoing political crisis.

Poland, the Baltic states, Romania and Slovakia have consistently opposed the project. Their opposition tends to be explained by a number of factors including strategic reasons (notably the loss of their current strategic importance as transit countries), the intention to diversify energy imports away from Russia, and concerns about being bypassed by the main flows of East-West energy trade. Long-standing fear of Russia, and of German-Russian cooperation, also play a role in Poland and the Baltic states. Slovakia also sees its substantial revenues from transit fees (€355 million in 2015) as being endangered.

On the other hand, Germany and Austria have emerged as the main advocates of the project. France and the Netherlands appear amenable to it as well due to the involvement of domestic corporate interests. The main argument that has been put forward to support the project is that it follows commercial logic by linking supplier and customers with competitively priced gas. It has been argued that Nord Stream 2 can provide cheap gas to compensate for dwindling North Sea gas production. It will also meet further demand that will stem from the closure of nuclear power plants in Germany and the need to switch energy consumption from more polluting coal and oil to gas.

Caught between opposing views at member-state level, EU institutions have taken different stances towards Nord Stream 2. For its part, the Commission opposed the project. In June 2017, it requested a mandate from the Council of the EU to negotiate an agreement with Russia concerning the operation of Nord Stream 2, arguing that it was necessary to define a legal framework. The request seemed to respond to pressure by member states opposing Nord Stream 2 and had the apparent goal of limiting Gazprom’s ability to use the pipeline’s capacity. However, the Legal Service of the Council concluded that there was no legal rationale for an EU-Russia agreement concerning the project. It also stated that the third energy package does not apply to the Nord Stream 2 pipeline.9

The reasoning of the Legal Service of the Council reflects existing precedents: pipelines from non-EU countries have been built in accordance with the United Nations Convention on the Law of the Sea, whereas the third energy package applies to pipelines within EU territory. In the case of Nord Stream 2, the package would apply to adjoining, land-based pipelines in the EU. Moreover, the EU energy market has been built around the principles of liberalisation and competition, and political attempts to block new projects run counter to this logic.

Following the Council’s response, the Commission proposed amending the third energy package in order to create a legal rationale for requesting the negotiating mandate. It is unlikely, however, that the Council will give the amendment the green light, which would require the support of a qualified majority.10 Even if it did, it would not provide a legal basis for stopping the construction of Nord Stream 2. The Commission’s initiative comes across as delaying tactics to placate member states that oppose the project. Given its clear political rationale, however, it runs the risk of making the dispute between EU institutions and between member states more acute.

To complicate matters further, the United States has intervened in the Nord Stream 2 debate through both Congress legislation and President Trump’s fiery rhetoric. Significantly, new draft legislation by Congress threatens to sanction European companies involved in Nord Stream 2. Similar legislation passed by Congress in the summer of 2017 led to a diplomatic argument with the German and Austrian governments, contending that the US extraterritorial sanctions were illegal and that ‘Europe’s energy supply network is Europe’s affair, not that of the United States of America’.11 Following negotiations with European diplomatic envoys, the 2017 legislation was softened with the addendum that sanctions would be imposed at the US president’s discretion in coordination with US allies.

Contrary to the 2017 bill, the new draft law could make the sanctions mandatory without requiring the approval of the US president or other coordination. Opponents of Nord Stream 2 see it as the last tool for attempting to stop the project. Conversely, supporters of the pipeline see the proposed extraterritorial sanctions as an illegal attempt to interfere in EU energy policy and promote US LNG exports as an alternative, regardless of their potentially higher cost for the EU and uncertainty about available volumes. Meanwhile, the laying of the Nord Stream 2 pipelines started during the summer of 2018.

Preserving Ukraine’s role in EU-Russia energy trade

Preserving Ukraine’s transit role in the EU-Russia relations is arguably the most politically pressing issue for the EU, in the light of new infrastructural projects. Ukraine has earned $2-3 billion a year from transit revenues, which are important to its economy. The construction of alternative pipelines could deprive Ukraine of this role, weakening it both financially and strategically vis-à-vis Russia.

The main question is whether Ukraine will be able to preserve its transit role after the current transit contract with Gazprom expires at the end of 2019. Ukrainian concerns increased in February 2018 when Gazprom stated that it would start a termination procedure for its supply and transit contracts with Ukraine. Gazprom’s statement was made in response to the outcome of a long-standing arbitration process concerning contracts with Ukraine’s state company Naftogaz.

After 2014, Gazprom and Naftogaz had filed claims against each other at the Arbitration Institute of the Stockholm Chamber of Commerce. The claims concerned the implementation of supply and transit contracts. A series of pronouncements left Gazprom with a net debt of $2.56 billion – a considerable sum, but only a fraction of what the two companies were claiming from each other. Gazprom stated that it wished to terminate the current gas transit agreement with Ukraine in this context, before arguing that it would use all legal means to challenge the outcome of the arbitration.

On closer inspection, Gazprom’s statement appears unlikely to have any concrete effects before the agreement reaches its expiry date in December 2019. As indicated above, in 2017 the company exported over 93 bcm of gas via Ukraine. In order to maintain these export volumes, Gazprom cannot manage without Ukrainian transit pipelines at present. In fact, this will hold true even if both Nord Stream 2 and the second line of TurkStream are built (which will take time, probably until after December 2019). Certainly, with these new projects becoming operational, gas volumes via Ukraine will diminish markedly, but they will not disappear.

Following Chancellor Angela Merkel’s request that Ukrainian pipelines remain operational, in April 2018, Gazprom itself has stated that at least 10–15 bcm/year will be exported via Ukraine.12 A larger export capacity via Ukraine will have to be maintained both to meet higher wintertime demand and to face the possibility of technical issues along the other routes. Southern European customers of Gazprom have also expressed a desire to continue their imports via Ukraine.

Hence, gas transit via Ukraine will almost certainly continue after 2019, but with smaller volumes than in the 2000s and 2010s. While transit volumes will diminish, it is also important to note that Ukraine is no longer as exposed to disruptions in gas supplies from Russia as it was in the past. Ukraine’s gas demand has fallen from around 65 bcm in 2011 to approximately 35 bcm in 2017. Most of the current demand is covered by domestic gas production and imports from the EU (even though the latter include reverse flows of Russian gas).13 This means that while Ukraine will probably lose most of its leverage as a key transit country, Russia has also lost much of its leverage over Ukraine’s energy security.

Conclusion: What to expect in 2018–19?

Several important developments will take place in EU-Russia gas relations up to the end of 2019. The construction of Nord Stream 2 will continue, while the Russian-Ukrainian transit contract will reach its expiry date. During this transitional phase, new tensions are to be expected until there is clarity on the volumes of gas that will be channelled through each transit route.

However, tensions can be alleviated if Russian, Ukrainian and European public and private stakeholders agree on keeping Ukrainian transit pipelines operational. Theoretically, this should not be difficult to achieve, as all sides need these pipelines in order to maintain the ongoing trade. The tripartite talks between the energy ministers of Russia, Ukraine and the European Commission, which are set to start in October 2018, should lead to an agreement on the post-2019 continuation of the Ukrainian gas transit.

From the Ukrainian and EU perspective, it will be more difficult to ensure that large volumes of gas continue to be channelled via Ukraine. Yet this is not impossible, provided that there is greater financial and entrepreneurial commitment (such as investments in the renovation of ageing pipelines) from those countries that see the Ukrainian route as a priority. Political statements and attempts to block other projects will not suffice.

On the other hand, the threat of US extraterritorial sanctions against EU energy companies risks widening the rift in transatlantic relations. What Washington could do, if it is concerned about Europe’s dependence on Russian gas, is to export its LNG to the continent and compete with Gazprom. The availability of multiple suppliers and the growing integration of the EU energy market would be decisive in reducing the scope for political uses of energy.

Endnotes

1 Gazprom Export, Delivery Statistics, http://www.gazpromexport.ru/en/statistics/. Last accessed 12 September 2018.

2 Anouk Honoré, Natural Gas Demand in Europe in 2017 and Short Term Expectations, OIES, April 2018, p. 1.

3 James Henderson and Jack Sharples, Gazprom in Europe – Two “Anni Mirabiles”, but can it continue?, OIES, March 2018, pp. 3–5.

4 Interfax Ukraine, Ukraine sees 13.7% rise in gas transit in 2017, 2 January 2018, https://en.interfax.com.ua/news/economic/474366.html. Last accessed 12 September 2018.

5 See Marco Siddi, The antitrust dispute between the European Commission and Gazprom: Towards an amicable deal, FIIA Comment, 25 April 2017, https://www.fiia.fi/en/publication/the-antitrust-dispute-between-the-european-commission-and-gazprom. Last accessed 12 September 2018.

6 See WTO, European Union and its Member States — Certain Measures Relating to the Energy Sector, https://www.wto.org/english/tratop_e/dispu_e/cases_e/ds476_e.htm. Last accessed 12 September 2018.

7 Marco Siddi, “The Arctic Route for Russian LNG Opens”, WE – World Energy, 9 May 2018, https://www.aboutenergy.com/en_IT/topics/arctic-route-for-russian-lng-opens.shtml. Last accessed 12 September 2018.

8 For a full analysis of the project, see Kai-Olaf Lang and Kirsten Westphal, Nord Stream 2 – A political and economic contextualisation, SWP Research Paper, March 2017.

9 For an in-depth discussion, see Katja Yafimava, The Council Legal Service’s assessment of the European Commission’s negotiating mandate and what it means for Nord Stream 2, OIES, October 2017.

10 A qualified majority is reached if two conditions are met: 55% of EU member states vote in favour, and they represent at least 65% of the total EU population.

11 German Foreign Office, Foreign Minister Gabriel and Austrian Federal Chancellor Kern on the imposition of Russia sanctions by the US Senate, Press Release 15 June 2017, https://www.auswaertiges-amt.de/en/newsroom/news/170615-kern-russland/290666. Last accessed 12 September 2018.

12 Reuters, Gazprom says gas transit via Ukraine to Europe may fall to 10-15 bcm per year, 10 April 2018, https://www.reuters.com/article/us-russia-ukraine-gas/gazprom-says-gas-transit-via-ukraine-to-europe-may-fall-to-10-15-bcm-per-year-idUSKBN1HH2HL. Last accessed 12 September 2018.

13 See Elena Mazneva, Russian Gas Return to Ukraine to Cost EU Traders $1 Billion, Bloomberg, 10 January 2018.